Portfolio Manager’s Monthly Update – September 2018

September 5, 2018

Dear Partners,

The U. S. oil and gas markets had a constructive month in August. Oil prices were firm, backed by a steady draw down of inventories and continued growth in worldwide demand. Economic and political conditions in many oil producing countries are chaotic. Looming sanctions in Iran add to the uncertainty of supplies. Prices are higher because demand is higher. Lost production, whether by depletion or by sanctions, must be replaced.

Over the past few weeks, the MLP market prices have improved. Numerous MLP partnerships have clarified capital structures making them more transparent to investors. Others have secured private equity investments to help fund the massive infrastructure projects that are needed to handle new production.

In the meantime, gas volumes are growing in areas such as the Marcellus and the Haynesville, while oil production is growing in the Bakken. Foreign offshore areas including West Africa, Guyana, and Brazil are also showing some life with higher oil prices stable. Much of the new U.S. supply of gas is flowing to export markets via LNG from both the East Coast and the Gulf Coast.

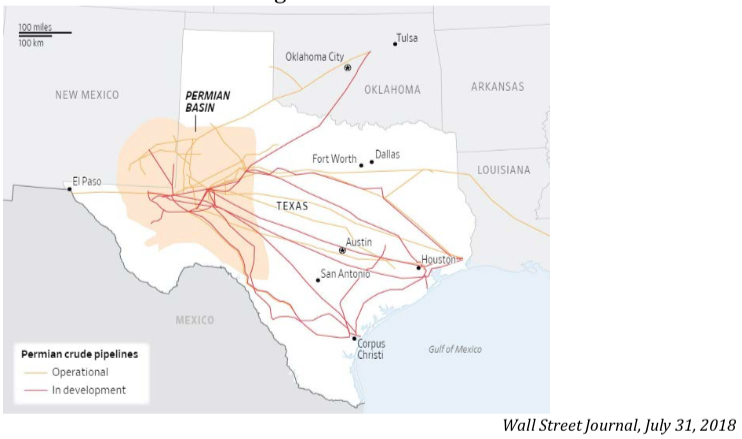

The real growth in domestic production, however, continues to be focused in the Permian Basin, where half of the working rigs are located. As I noted in last month’s newsletter, a potential future take-away shortage might develop as production growth could outpace pipeline take-away capacity. However, we think that even if production in the Permian doubles in five years, take-away capacity should be able to increase to handle the growth in production. This is demonstrated in the map from last month’s newsletter and shown again below:

Another issue has been brought further into the light recently – the large and increasing amount of produced water from the Delaware side of the Permian Basin. The energy industry has long known that the amount of produced water would be a major issue and the key players have made allowances for how to handle it. For those who do not have a plan, it will be a major problem. To demonstrate the scale of what is to come, imagine each well in the Delaware that produces 1000 bbl./day of oil will also produce 5000 bbl./day of water. It is a problem that will reduce profit margins for many producers.

Taking a step back to look at the policy/geopolitical outlook, U.S. policy decisions seem well grounded in both economic and common sense terms. Many positive developments are largely ignored by the press. I see the current hardball approach as aimed not at producing a long term trade war, but as a tactic meant to create a much better world and much more free trade for everyone. Those who deal with a rogue Iran as it is now (an indisputable bad actor for more than a generation) and complain of U.S. interference should imagine how much business they might do with a more reasonable government in place in Iran. This appears to me to be the aim of U. S. policy. Nobody wins a trade war and we do not believe the U.S. wants one. The administration seems to want trade practices that match the modern world. Many of the trade practices put in place after WWII are no longer in the best interest of the U.S. Now allies and enemies alike are facing a very different America.

U. S. markets are optimistic. Energy markets are stable. Stocks are at all-time highs. The U.S. economy is growing well and unemployment is at record lows for all groups of people. In the current economic scenario, we are confident that our energy strategy is the right one for our investors.

Yours Truly,

Dana McGinnis &

Mission Advisors